What we bought: How YNAB gives me peace of mind and keeps my money in check

Four years, one house and a wedding later and I’m still using this budgeting app on the daily.

We may receive a commission on purchases made from links.

I've always been pretty money-conscious, but I didn't really get into budgeting until I was in my mid-twenties. "Budgeting" is generous — I thought I was budgeting, but really I was using a crude Google Sheet system to track my expenses every month. I didn't truly understand the difference between those two things until I started looking into ways to upgrade. It had been working fine for me, but as I got older and wanted to grow my savings, save up for a home down payment and a wedding and generally do more "adult" things with my money, I started to scour the internet for alternatives. I settled on You Need a Budget (YNAB) about four years ago and I've enjoyed it so much that I keep using it even after achieving some of those milestones.

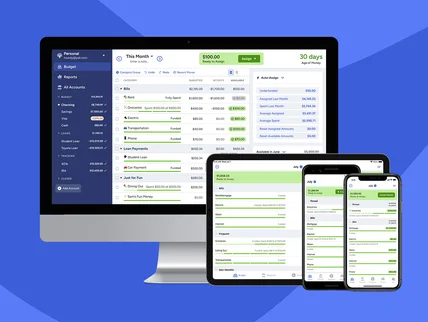

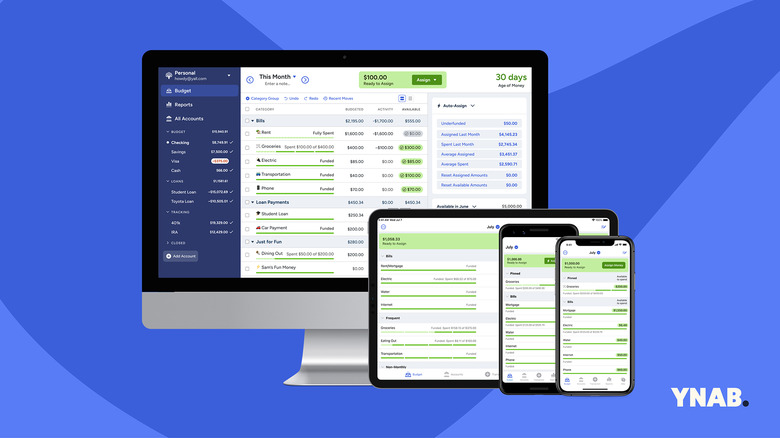

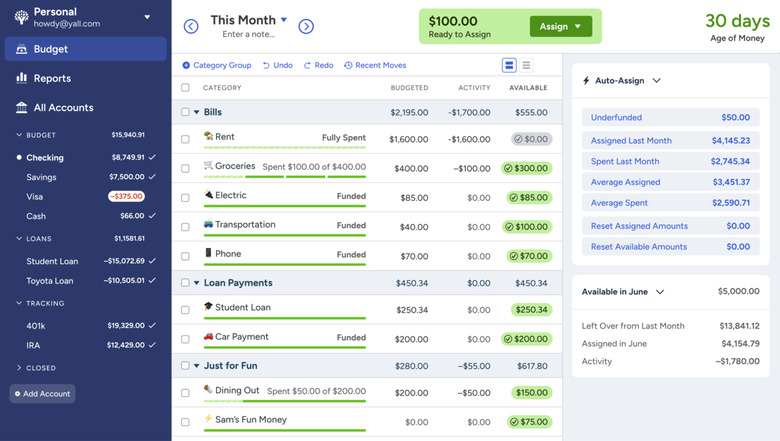

The YNAB Method is an approach to budgeting that resonated with me then and still does today. I won't belabor the basics here, but put simply, you're to give every dollar a "job" as soon as you get paid by taking care of immediate needs first and then accounting for the rest of your true expenses. The way YNAB does this is basically by acting like a digital envelope system where you can customize all of your envelopes (or "categories") and the amount of money you need for each ("targets"), and dump money into all of them every time you get paid. For example, I know I need $65 each month to pay for internet, so I have an internet category in YNAB with a target of $65 each month that's due by the 15th, since I'll need that money to pay the bill on the 20th of every month.

Follow that example for all of the rest of your expenses like rent or mortgage payments, groceries, electricity, insurance premiums and you'll have a full YNAB budget in place. You can (and should) also do that for "true" expenses, which include things like hair cuts and car maintenance in the YNAB system. You may not need a specific amount of money for things like that every month, but you can plan for them by saving a little every time you get paid — so by the time you need to get that hair cut ahead of a wedding or unexpectedly need a new set of tires, you have at least some, if not all, of the money necessary to pay it.

I was already taking stock of my standard expenses and setting aside money for those first and foremost, but YNAB made the process much easier. It's worth noting that was already part of my routine. I was privileged enough to get a decent financial education from my parents growing up (mantras like "pay yourself first" come to mind, and I see taking care of your most necessary expenses as a way of accomplishing that).

The game-changer for me was considering my "true expenses," which added up quickly. The inevitable weekly takeout order, veterinary bills for our cat, train and rideshare fees and the like were all things I knew I needed to pay for but didn't previously deal with until the time came. In YNAB, you can create categories for all true expenses and plan for them each month (or week, depending on how you budget/get paid) so there's (hopefully) never a question of how you're going to pay for any of them.

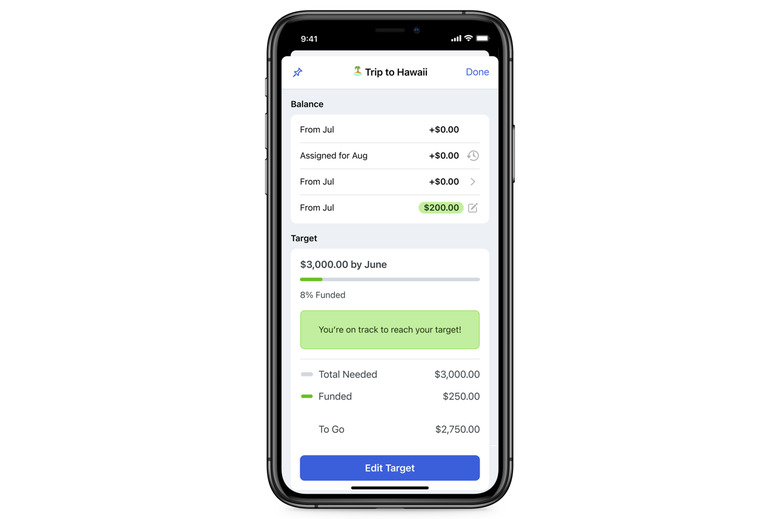

If you're able to do this and get your expenses in order, it's possible that you'll find you have money left over each paycheck. Then you can expand your budget to think about other true expenses or sinking funds you may want to address. My line between true expenses and sinking funds is blurry at best, but the latter are just allocated monies you set aside for variable expenses that you know are inevitable like home maintenance or insurance premiums.

Holiday gifts were big for me; every year, I have even more people in my life that I need to buy gifts for during the holiday season and I never planned for that in advance before using YNAB. Now, I have a "holiday gifts" category with a generous target that I put money toward every month and set to be "due" every year in early October. As soon as sales start to kick in during the fall, I have a pool of money with which I can buy all of my loved ones' gifts.

I should say that YNAB appeals to my Type-A, über-organized personality, but you can't plan for everything. A few years back, I unexpectedly had to spend about $500 for some car repairs and I didn't have quite that much in my "car maintenance" sinking fund. Instead of panicking, I moved some money over from my "clothing" category to cover the remainder of the costs. It was a bit painful psychologically (I love seeing those little green progress bars in the YNAB app), but it didn't impact my finances at all. YNAB accounts only for the money you actually have, regardless of which category it's in, so I wasn't spending anything that I couldn't afford. That's really important to me, as someone who tries to live within their means — and as much as possible, below it — to avoid lifestyle creep.

Getting back to those "adult" priorities I mentioned before: YNAB was one of the key things that helped me and my partner save up a home down payment and the funds we'd need to pay for our wedding simultaneously, without feeling too stretched along the way. We cut down (not cut out, mind you) on all unnecessary expenses and aggressively saved during this five-year period, and YNAB made keeping track of it all easy.

But I would like to stress that the service was just one of the things that helped, and there were other factors that contributed as well. It's not realistic to suggest budgeting alone is the answer to all of one's money prayers. But it's certainly a step in the right direction and a good habit to build over time.

I consider YNAB up there with 1Password as one of the few services I'm happy to pay for every year because of how much it adds to my life. However, it's worth noting that you don't have to pay for YNAB to start budgeting using its tenants. The YNAB method, the envelope system and zero-based budgeting are all very similar and you can do them all with less expensive tools, and even manually with physical envelopes and cash. There are plenty of online communities with flourishing examples of how you can get started without paying for yet another subscription. I recommend checking out Taylor Budgets, Budget Treasures and other similar YouTube channels for more inspiration.