The Coin universal card is ready for 2012

If your wallet is bursting at the seams with credit, gift and loyalty plastic, the Coin universal card is supposed to lighten the load. Just add all your information to the app, sync it with Coin and get ready to buy all the things with a swipe or an NFC tap. Except when you can't. While the premise and feature set are intriguing, and in some cases helpful, in practice, it feels like too little too late. With Apple Pay, Android Pay. Samsung Pay and others already working on the future of transactions, Coin might have missed the boat.

The $124 (currently $99 for a limited time) smart-credit card replacement has been plagued almost from the beginning. From the typical delays common with crowd-funded devices, to missing the eventual chip and PIN changeover. With Coin 2.0, the company hopes it can get back on track by actually shipping a product and integrating EMV-NFC for wireless, but secure, chip and PIN support. Unfortunately, there are still some issues it needs to sort out.

After adding four cards (debit, company, gift and credit) to the Coin with the supplied reader, I went shopping. Buying juice at Walgreens with my debit card went off without a hitch. Paying for parking with my company Visa was simple. And finally, I used that $25 gift card while shopping at Target without a problem. But that Target shopping trip also revealed that Coin wasn't ready replace my debit card entirely.

The Target in San Francisco uses chip and PIN terminals now. While NFC with EMV should have solved the problem, it turns out Coin has only made a deal with Chase bank. My Bank of America debit card isn't currently supported. No NFC and no chip meant I had to dig out my actual debit card. To be fair, Coin says it's working on securing deals with major banks. That's great, but it also means while that's happening, I have to keep at least one of my cards in my wallet. I found an issue, a fix is coming (eventually), end of story. Right?

Unfortunately it wasn't. Even at stores that had swipe terminals, my debit card on the Coin didn't always work. The employee would swipe it a few times, stare at the card, look at me, then swipe a few more times before handing it back to me. I'd shrug and pull out my Bank of America card. It worked on the first swipe every time. A lot of these incidents happened at local businesses with older POS (Point of Sale) machines. But if the swipe worked with the original card, it should have worked with the Coin. After a week, the Coin failed to complete about 25 percent of the Bank of America account transactions.

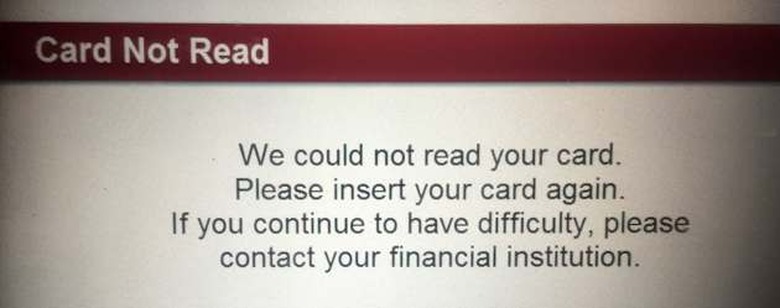

The biggest failure came at the ATM. The machine couldn't read the card. At that point, it was clear that a card from one the nation's largest banks couldn't be replaced by Coin. I fully expect Bank of America to get onboard the Coin bandwagon along with Chase. But, it's difficult to recommend something that's supposed to clear out your wallet, when at the moment it's not ready for many of its potential customers.

Plus, gaining new customers is going to be tough with more and more companies adding payment solutions to the phones we already have in our pockets. Coin's security is great with a card that locks after each use, is password protected and displays the last place it was used on a map in the app. But your phone has a lock screen and can be found when misplaced with services like Find my iPhone. Additionally services like Apple Pay use one-time-use tokens instead of your card's number protecting you in case a merchant gets hacked. Of course these all work on NFC and swipe is still the preferred method of payment in the United States.

What this means is that your wallet isn't going to get much slimmer any time soon. Coin would have been great a few years ago if it worked all the time. If you can't put your faith in a payment solution 100 percent of the time, it's not ready for your wallet.