mobilepayments

Latest

Apple is reportedly teaming up with American Express on iPhone payments (update: MasterCard too)

Those longstanding rumors of Apple building a mobile payment service may be coming true sooner than you think. Recode's sources claim that the folks in Cupertino have struck a deal with American Express to work on an iPhone payment system, hot on the heels of The Information's report of a similar agreement with Visa. Details of the system aren't clear beyond a tie-in with the next iPhone (and likely your iTunes account), but Apple is supposedly ready to spill the beans at its September 9th event -- if the leak is accurate, you're going to get the full story pretty quickly.

Apple's new iPhone might really, seriously have NFC this time (maybe)

Smartphone prognosticators have claimed for years that the next iPhone would have NFC for mobile payments, and for years they've written follow-ups explaining why it never happened. As always, there's plenty of NFC smoke in the air, but is there actually a fire? A new report from Wired's Gadget Lab says yes - according to the usual unnamed sources, Apple's going to show off a shiny new mobile payments platform at its September 9 event (we're still waiting for our invite) and NFC is expected to play a part. Just how big a part remains shrouded in mystery -- after all, Apple SVP Phil Schiller said at an AllThingsD event that NFC wasn't a solution to any current problem consumers faced.

PayPal's One Touch wants to power your in-app mobile purchases

It's a pretty common thing to see in an online store: pay with PayPal -- but what about on mobile devices? Well, the eBay-owned company is working on that. The company just announced PayPal One Touch, a new system that (as the name implies) hopes to make paying of items in mobile apps a one-touch affair. The feature isn't an app itself, but rather a service that can be embedded in other apps. Users will log into their PayPal account one time, and subsequently be able to pay for products in supported apps with a single click.

Shift's debit card lets you pay with both real and virtual money

Part of the challenge of Bitcoin and other virtual currencies has simply been the need to juggle different apps and cards to use every payment option at your disposal. Wouldn't it be nice if one card could handle everything? You might just get your wish. Shift Payments is testing a new debit card that can switch between real and virtual money on the spot, such as through an app; you could pay for morning coffee with Bitcoin and after-work groceries using real cash. Loyalty card support is in the works, too.

Square's new chip card reader will make your payments more secure

There's a good reason you don't usually see Square readers outside of the US: they're built to read payment cards with magnetic stripes, not the more secure chip-and-PIN cards that are common everywhere else. All that's set to change, however. Square has revealed plans for a reader that accepts the chip-based EMV format alongside stripes, letting shops handle credit and debit cards from around the world (and the US, once it catches up). The company will only start taking pre-orders for the payment device later this year, but it could be worthwhile for stores and customers alike. Besides the greater availability, it's much harder to clone a chip card -- you shouldn't have to worry about an unscrupulous clerk (or a clever hacker) stealing your credit card and going on a shopping spree.

Starbucks wants you to use its app for payments in other stores

Starbucks' mobile apps could soon let you buy much more than your next grande latte. The coffee shop's digital lead, Adam Brotman, tells Recode that the coffee shop giant is talking to companies about using its app for payments and loyalty programs in other stores. He's not naming any would-be allies, but the strategy would turn a fairly ordinary restaurant app into more of a universal digital wallet that just happens to focus on drinks. And even if that doesn't pan out, Starbucks is still committed to expanding the role of its software -- it's determined to offer coffee pre-orders across the US, regardless how long it takes to make the feature work.

Isis mobile payment platform to change its name to avoid association with militant group

Near the end of 2010, a group of telecommunications and commerce businesses joined forces to form a mobile payment venture called Isis. It was a solid brand name: Short, simple and easy to remember. Unfortunately, ISIS is now associated with a militant group based in the Middle East, so the wireless company believes a branding tweak makes sense. In a blog post, CEO Michael Abbott explained: "However coincidental, we have no interest in sharing a name with a group whose name has become synonymous with violence and our hearts go out to those who are suffering. As a company, we have made the decision to rebrand." Abbott didn't announce what the new brand would be -- we imagine that he's working on that as we speak -- but mentioned that he'd have more information to share in the coming months.

Paym platform for sending and receiving money by mobile number goes live

Paym, a new mobile payment platform that lets you send money to a mate for your share of Friday's curry with only their phone number to hand, is now live in the UK. To use Paym, you'll first need to associate your mobile number with your UK bank account either online or through your bank's mobile app. Once that's done, you can send or receive money (up to £250) from anyone that's also signed up to Paym using nothing but mobile numbers. The process may sound familiar, as Barclay's Pingit app has been capable of the same thing, regardless of which bank you're allied with, since it launched in 2012. The only real difference with Paym is that it's integrated into the systems and apps of other banks, making it a bit more visible, and convenient. Most well-known banks and building societies support Paym at launch, with the only notable exceptions being the Royal Bank of Scotland and NatWest, which are expected to join up sometime this year, and Nationwide, which'll wait until early 2015 to adopt Paym. Until then, though, anyone with unsupported accounts can still use Pingit, so no excuses as to why you can't contribute towards the cab fare.

Swedish students cook up a way to pay with your hands

Big companies have been trying to make in-store payments with mobile devices a thing for years, which makes Frederik Leifland's approach awfully refreshing by comparison. There's no smartphone, no NFC chip, no apps involved here -- all you need to pay for your Frosted Flakes and Nutella is the palm of your hand. You see, Leifland (of Sweden's Lund University) has cooked up a way to identify shoppers by the unique branching pattern of veins in their hands.

Wendy's now lets you pay for a meal with its mobile app

Wendy's, home to a bunch of square burgers and Frosty, is following in Burger King's footsteps and embracing mobile payments. Now, you can use the Ohio company's app to pay for your purchase in most (but not all) of its locations in the US. Just like its Burger King counterpart, the app acts as sort of a digital wallet that generates six-digit codes you'll have to give to cashiers for payment. Wendy's, however, has regrettably left out one of the BK app's best features -- discounts and coupons. The fast food chain apparently decided to offer mobile payments in an effort to attract the younger, smartphone-obsessed set. Unfortunately, the app's limited features (you can't use it to call in a delivery, if you're wondering!) and lack of discounts as a perk make it a less convincing download than its competitors. But, hey, at least it can show nutritional values, so you don't scarf down a Baconator without knowing it has 940 calories.

Burger King gets appy with new mobile payment product

Burger King, the perennial Pepsi to McDonald's Coke, is technologizing with a mobile app. But before you get out the pitchforks and cry "diabetes! laziness! obesity!," it's important we mention that this app, set to launch in limited locations next month with a nationwide rollout shortly after, is not like Seamless. That is, you can't order Burger King for delivery -- not yet, anyway. As Bloomberg reports, this Burger King mobile app comes by way of Tillster, a company dedicated to facilitating digital ordering for big name fast food clients like KFC, Subway and Pizza Hut. The app's more a virtual wallet than anything at this point, letting users pay for orders by adding funds to a virtual card. Although, the company has stated there's potential for new features to be added at a later date, like placing an order for pick-up (yes, really). As a mobile payment option, the BK app's not all that compelling of an idea, until you factor in the accessible nutritional information and coupon offers for discounted meals and items. You know, a little incentive for the young'uns that eat Burger King; a little something to make that value menu even cheaper, if that's even possible. [Image credit: Getty]

MasterCard and Visa users may soon flip the switch on KitKat NFC payments

With a consumer reception that could be described as lukewarm at best, mobile payments haven't exactly been a raging success. Despite Google's efforts, Wallet failed to take off, while Isis also continues to struggle, despite support from major US carriers. Now, MasterCard and Visa are readying yet another potential solution, this time tapping the new Host Card Emulation (HCE) support in Android 4.4. The service, which is only supported in NFC-enabled KitKat phones, stores credit card info remotely rather than on an embedded "secure element," expanding compatibility beyond pre-approved apps. With HCE, when you go to make a payment, your phone will transfer credit card data directly to the NFC terminal, without storing it in your handset. MasterCard and Visa are both working to finalize the specification, following various trials over the last few months. Ideally, a significant number of credit card holders will be able to take advantage of HCE-enabled payments beginning later in 2014, with more details to come in the first half of this year. (AP Photo/Manu Fernandez)

Google Wallet will make collecting loyalty points easier and noisier

Early adopters of mobile wallet services are brave enough to hand over the keys to their finances in the name of convenience. When you're signed up to a plethora of loyalty schemes, though, inputting all these details before ditching the plastic could be quite the opposite. Google doesn't want you burdened with such tasks, and in an impending update to its Wallet app for Android, has said it'll introduce a new feature that adds loyalty cards with one click of your smartphone's camera shutter. A natural progression from the recent recognition feature that adds debit and credit card details in the same way, snap a picture of your loyalty card and Wallet will do the rest. Furthermore, when you're near a store with which you have a card, you'll get a notification to remind you (that Google knows all). While the Android app was updated yesterday, there's no mention of these additions, so we'll take Big G's word that it's "rolling out this week." No news on when an update could hit the iOS version of the app, but as Wallet only launched on the platform a few months ago, we're not going to hold our breath.

Amazon might launch Kindle-powered checkout system and cloud-based payment service

Amazon might still be working away on its far-out delivery drone project, but it's also reportedly cooking up something else, admittedly a little tamer, too: a Kindle checkout system and a P2P payment service. Yes, the former's exactly what it sounds like -- a Kindle tablet equipped with proprietary software and a credit card reader (like Square), at least according to the Wall Street Journal. Amazon supposedly acquired GoPago (a mobile payment platform for merchants) in 2013 to nudge this venture forward, though TechCrunch says it's not the only payment solution the firm's developing. Apparently, the company's also creating a cloud-based P2P payment system that might be accessible not just on mobile phones, but also on desktops, making it a veritable PayPal competitor. We just hope it doesn't tie up with Amazon's plans to "ship before you buy" if it does launch, because surprise credit card charges are a nightmare.

Apple is reportedly building a mobile payment service

There are plenty of existing mobile payment systems that let you buy goods with your iPhone, but there are now signs that Apple wants to take on some of those duties itself. The Wall Street Journal claims that the company is in the early stages of building a mobile payment infrastructure that would let its customers buy all kinds of products and services, not just those in its own stores. Sources say that Cupertino has tasked the former head of its online store with getting the service off the ground, and it's reportedly discussing the idea with other companies in the tech industry. Apple isn't commenting on the rumor, but it has been researching mobile payments for years -- we know it's at least intrigued by the concept.

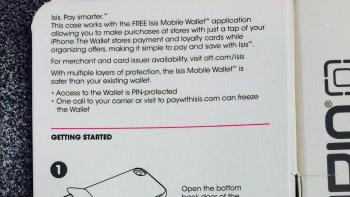

This case will turn your iPhone into a mobile wallet for $70

After a brief tease earlier this week, Incipio has officially unveiled its iPhone mobile payment case. The Cashwrap Mobile Wallet gives most iPhone users NFC payment support at any place that accepts Isis; beyond the case, all you need is a compatible account and a free app. If you're eager to stop paying with plastic cards, the Cashwrap should be available online for $70. AT&T is only due to launch the peripheral at retail on January 31st, although the recent in-store sighting hints that you might have a chance at scoring a retail unit ahead of schedule.

Isis Mobile Wallet now supports Wells Fargo Visa credit cards

Isis -- a joint mobile payment venture between AT&T, T-Mobile and Verizon -- has partnered up with banking juggernaut Wells Fargo, shortly after it rolled out nationwide. In addition to Chase, American Express, J.P. Morgan and random loyalty cards, users can now load their mobile wallets with Wells Fargo's Visa consumer credit cards. This allows them to purchase from participating merchants (there are "hundreds of thousands," according to the bank) that accept NFC payments without having to bring their plastic to the store. Want to use the system, but don't know where to begin? First things first: Make sure you have an Isis-ready Android smartphone from any of the three aforementioned carriers. Once you've received the special SIM and have activated the service, you can start going on nighttime trips to McD's or doing emergency CVS runs with only a phone in hand.

Isis nationwide rollout is now available for AT&T, T-Mobile and Verizon customers

After announcing plans for nationwide deployment back in July, and nabbing commitments from both Chase and American Express in the process, Isis is now available for the masses. Customers on AT&T, T-Mobile and Verizon who wield one of over 40 capable handsets can snag a free enhanced SIM and download the app via Google Play to begin using the mobile wallet in all of its NFC payment glory. Of course, in addition to credit and debit cards, the platform also supports loyalty cards, so free drinks at vending machines thanks to MyCokeRewards are a swipe away. How's that for an afternoon pick-me-up?

Pantech Vega LTE-A gains fingerprint-based mobile payments

Want to find a nifty use for the fingerprint sensor on the Pantech Vega LTE-A? Well, thanks to the hard work of two South Korean companies, it's picking up the ability to pay for goods by authenticating with your fingerprint. This news comes from Danal, a mobile payment provider, which tapped the fingerprint technologies of Crucialtec to create the BarTong app. While the concept of fingerprint-based payments isn't entirely new, it's claimed to be an industry first for the mobile phone. The BarTong app is currently exclusive to South Korea, but its creator is looking to expand the payment service into the US and China. Naturally, Danal may want to hold off until fingerprint readers become more widespread in smartphones, but we certainly won't fault the company for being ambitious.

Apple is silently telling us to stop asking for near-field communication

We've been hearing rumors about an NFC-enabled iPhone and/or iPad for years now, and the song is always the same: "Sources say the next iDevice will have NFC, and it's about time!" Yet here we sit, with a pair of new iPhones just a day from launch, and no NFC in sight. If there's anything the iPhone 5s and AirDrop should tell us, it's that we should stop expecting an Apple smartphone or tablet with near-field communication, at least for a while. NFC speaks two languages It's important to separate the two primary uses for NFC: Sharing and payments. NFC mobile sharing is useful for everything from virtually handing documents to a coworker, to (apparently) getting naughty videos from your spouse before a business trip. This is an NFC feature that can be used by the widest range of people, and all that is needed is two individuals with compatible devices. NFC payments are quite different -- not in how it works, but in how useful it really is. Finding retailers that accept NFC payments isn't exactly easy. If you don't live in a place like San Francisco or New York City, the ability to use a virtual credit card on your smartphone isn't just a rarity; it's barely even an option. I know this because I live in a midwestern city where people will line up overnight for a new Nexus or Galaxy smartphone, but if you asked a cashier at local store if they accept Google Wallet they'd stare are you like you were from another planet. AirDrop uses Bluetooth and ad-hoc WiFi rather than near-field communication, but it accomplishes the same feat when it comes to mobile sharing. If you have an iPhone 5, 5s, or 5c (or 4th gen iPad, 5th gen iPod, or iPad mini), you can share files with other compatible devices simply by selecting the file and the recipient. It's a no-setup, no-hassle way to send files locally, and you don't need to smash your phones together to make it work. With AirDrop, Apple has duplicated the most useful feature of near-field communication without buckling and including NFC technology in its new devices. Buy why? Apple isn't on board the NFC train, but why? It could be that the technology doesn't seem secure enough to bet on, or that with so few merchants accepting NFC, including it wouldn't actually pay off. In the end, it's almost certainly a mix of many factors, but one angle I don't see mentioned very often is that by adopting near-field communication, Apple might be helping its competitors more than itself. I don't think it's hard to argue that if the new iPhone 5s and 5c included NFC, merchants would have a much greater incentive to invest in the technology. This could benefit Apple, of course, but it would boost long-suffering NFC stalwarts such as Google Wallet (which, ironically, just launched a non-NFC iOS app today) even more. NFC is struggling and growth is slow. By refusing to include it in new devices, Apple is certainly not doing it any favors -- in fact, without an iDevice in its corner, NFC may never break into the mainstream. That's a powerful position for Apple to be in, and one they won't be in a hurry to give up. Will we ever see an NFC-enabled iDevice? It's not entirely out of the question. Apple already has patents on the books that would use near-field communication for sharing, though the systems described work much like AirDrop already does but substitutes Bluetooth for NFC. Regardless, Apple already has everything it needs to wage a long war against near-field communication if it chooses to. With AirDrop handling the local sharing, Passbook acting as a go-between for things such as gift cards and event passes, and a retail scene where NFC is still a non-factor, there's almost no reason to even consider it.